As a founder, building a startup feels like pushing a rock uphill. Frustrating, exhausting, relentless, uncertain.

If you don’t give up (and you get lucky), at some point you’ll finally start to show some signs of product-market fit. Great! It’s finally working.

At this point, you’re probably pretty tired, so it’s natural to want to rest from pushing the rock uphill, at least for a bit. You might now raise another venture round, based on the traction you’re seeing.

You’ll likely start to build out your team. You have something repeatable that you can scale with more people and, if you raise money, you also have the budget.

The new team members aren’t like the very early team members. The new folks are probably more professional, and more experienced. They have playbooks. They start to do what you ask them to do: turn the success you’ve found into a repeatable and predictable process to continue to scale revenue.

You have a working company that is growing. It should be celebrated.

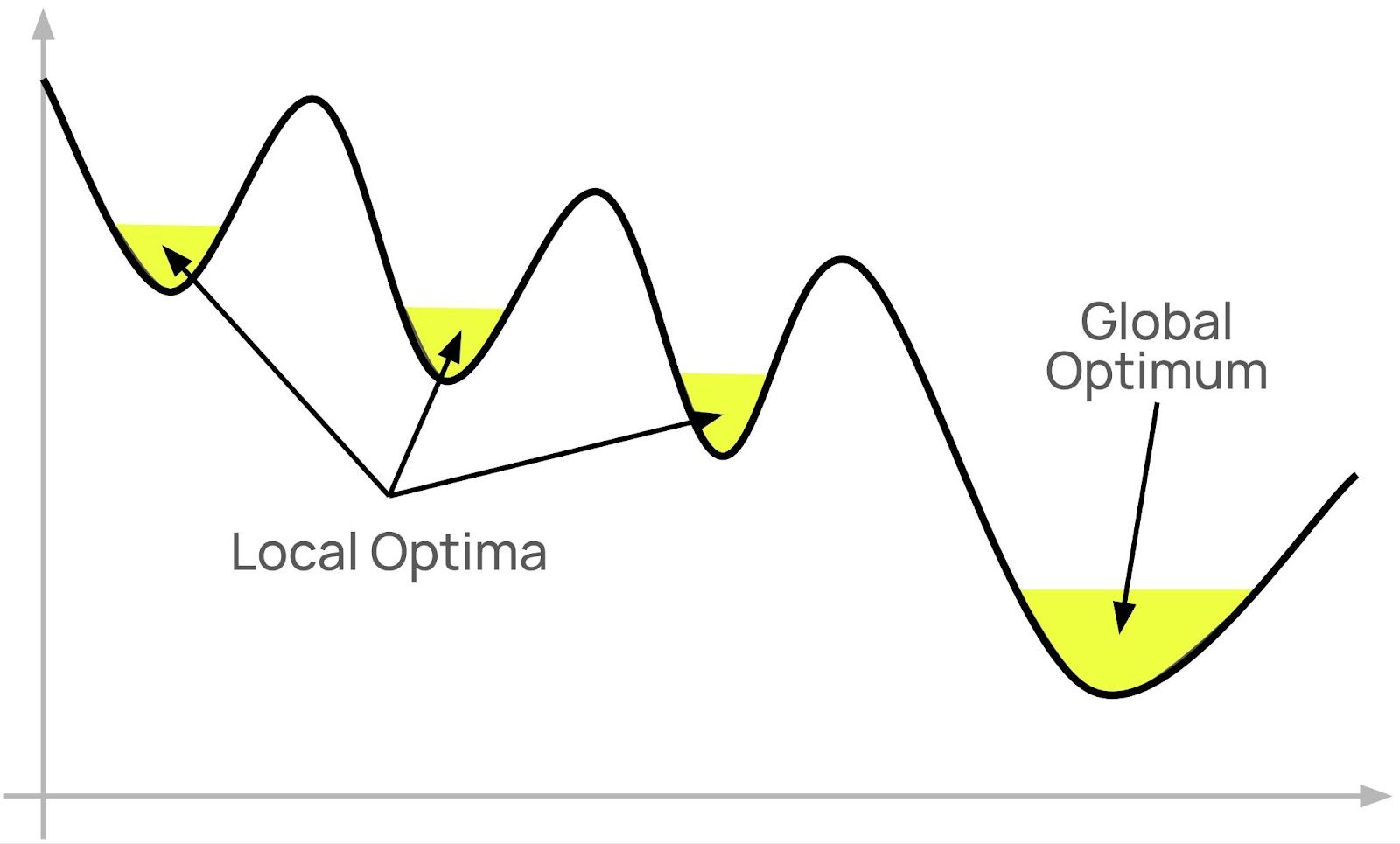

The problem is that you don’t know if you’ve found your global optimum or merely a local optimum.

Could there be an even better market, business model, product, and/or customer out there if you just keep looking; if you just keep pushing the rock uphill?

Many startups get stuck in these local optima. Why is it hard to escape them?

Firstly, everyone is telling you how important it is to focus. Do one thing well, rather than several things poorly. Great advice.

Secondly, you can unintentionally create the very inertia that keeps you stuck in the local optimum. All those people you hired once you got something working are there to maintain the local optimum: to make what’s working keep working. In fact, their jobs arguably depend on staying in the local optimum. So, they are unlikely advocates of trying something different.

There are also underlying cognitive biases at play here. Kahneman and Tversky wrote about “loss aversion” – the tendency to worry more about what you might lose from a change versus what you might gain. Others have written about “psychological inertia” and the “status quo bias”.

All of this happens against the backdrop of founders being bombarded with suggestions (many unsolicited) of things they might improve or do differently, competitors that are having success with a different model, new enablers that might be tried, etc.

I have some advice for both founders and investors on tackling this local vs global optimum challenge.

Founders:

Remain open to the idea that you may not yet have found the global optimum for your company, even when things seem to be going relatively well.

Reserve some mental bandwidth and resources for the ongoing pursuit of a global optimum. The whole point of a local optimum is that it takes initial effort to get out of it before you can continue to a better place. Conduct small experiments to explore options that may find better optima.

Be rigorously data-driven. To make sure you are comparing apples-to-apples, make sure you are comparing unit economics between options. I would argue that the Y-axis on the chart above should be CAC doubling time.

Investors:

Before sharing suggestions for other areas or models that a founder might explore, be clear on whether you think they genuinely present the opportunity to find a global optimum, versus just sharing to appear useful.

Be specific – explain why you’re sharing and describe how a change might get the founder to (or close to) the global optimum.

By the way, the seeking of global optima is precisely what the underlying algorithms at the heart of machine learning and AI are doing. It is a process called “gradient descent” and there are many nice visualizations of how it works. (e.g. https://medium.com/@gallettilance/gradient-descent-a89dbe1affe4) It’s fascinating to see how the algorithm is “putting out feelers” from each optimum it finds in the search for the global optimum, just like I am advising founders to do.

If you haven’t, I bet you’ve at least watched someone struggle with it.

You yank on the starter cord with all your might and…nothing happens. You try it again…still nothing. After a few more tries, you’re sweaty and frustrated. But the grass still needs cutting.

You keep trying.

Three more pulls. Still nothing. You curse and kick the mower.

What’s wrong? Are you not pulling hard enough? Are you not strong enough? Or, is something else wrong?

Next time, you pull the cord and the motor fires. But, just briefly. It quickly stutters out again. Progress of a kind.

Finally, you realize that there’s not enough gas in the tank. Once you top it off, a few more pulls and you’re mowing grass!

This is what starting a company is like. Except slower.

With a startup, each pull of the starter cord is equally tiring. But, each pull can take weeks.

You don’t know how many pulls are going to be needed. You don’t know if it’s ever going to start working.

You just have to keep pulling, and keep tweaking things. Just like the mower, sometimes it will start but then, quickly stop again. It’s just as frustrating but for much longer.

This is why founders need grit to keep pulling. They also need smarts to work out why it’s not working.

But, there’s a better way than struggling alone. What if you had an experienced team to help? A team of lawnmower experts who were there to check there’s enough gas in the tank, to top it off if there isn’t, to make sure the spark plug is not fouled, to make sure the blade is adjusted correctly, or just grab the cord and pull with you.

That’s what a Venture Studio does. A Venture Studio helps you start the lawnmower so you can start mowing.

At Platform Venture Studio, we’re helping the next generation of entrepreneurs start their lawnmowers. If you’ve ever thought about being a startup founder yourself, or just want to checkout the companies we’re building, please consider joining Platform.

This is Part 2 of “Everything You Always Wanted to Know about Unit Economics but were Afraid to Ask”.

This part covers the Unit Economics of Two-sided Marketplaces. If you need an introduction (or refresher) on Unit Economics, please read Part 1 first.

Definition

Firstly, let’s define two-sided marketplaces: these are businesses that make money by connecting Supply with Demand. Examples are Wonolo, Uber, eBay, and Airbnb.

Sometimes, which side is “Supply” versus “Demand” can be counterintuitive. To make it simple, Demand is normally the side that pays the money. The marketplace business collects that money, takes out its slice, and passes the rest of the money to the Supply side.

At Wonolo, our “Supply” is our Wonoloers (the workers who do the job) and our “Demand” is our customers (companies that pay money to have the work done).

For Uber’s core business, riders are the “Demand”, and “Supply” are the drivers and their cars. For Airbnb, “Demand” are guests and “Supply” are hosts with properties.

Unit Economics

Unit Economics get tricky in two-sided marketplaces because you have to consider both Demand and Supply.

To start with, you have two acquisition funnels, two CACs, two LTVs, two Break-even Points, etc. You also have marketplace effects to consider.

This provides for a number of possible approaches to understanding Unit Economics:

model Supply and Demand in isolation,

model the Demand side as your “unit”, and consider Supply-side costs as variable costs,

model your Supply side as your “unit”, and consider Demand-side costs as variable costs, or

combine Supply and Demand and model at the individual interaction level – e.g. your unit is a job (Wonolo), ride (Uber), or stay (Airbnb).

In practice, you will often end up doing all of the above to provide multiple perspectives to investors.

However, for simplicity, my strong recommendation is that you start with modeling your Demand side as your “unit”. I find that this is the most intuitive for most cases. It most closely resembles the modeling of Unit Economics for simpler SaaS businesses, which are what most investors are familiar with.

Extra Layers of Complexity

In addition to considering how to model Supply and Demand, many marketplace businesses have additional complexities which make their Unit Economics even harder to model.

These complexities are not unique to marketplaces but are seen in many of them:

Variable spend: unlike a simple SaaS business, where customers sign-up and pay a fixed amount each month (MRR), marketplace users can have highly variable spend month-to-month. This has large impacts on LTV and break-even, and can make averages misleading.

Variable pricing: often the fee that customers pay is negotiated and/or variable, meaning margin is variable.

Seasonality: if a business is seasonal, it means the Break-even Point depends on when in the year a customer signs-up. This makes it hard to compare cohorts.

Ambiguous churn: for a simple SaaS business, customers sign up and then pay every month until they explicitly cancel their service. In contrast, many marketplaces only make money when supply and demand transact. Either or both sides can go dormant at any time and then come back at any time. This makes modeling churn hard and churn is a big determinant for LTV.

There are various ways to cut through these complexities, including comparing cohorts of like customers, and seasonal adjustments, but I’ll save those for a potential Part 3.

Marketplace Example: Wonolo

Since Wonolo is a business I’m intimately familiar with, I’m going to use it as my example. However, the concepts here will be very similar for any two-sided marketplace.

Note: the numbers I’m using here are for illustrative purposes only, and to make for simple math. Several details that have a smaller impact on the numbers are omitted for simplicity.

Demand-side

Per the above, we’re going to model our Demand-side first.

Demand-side CAC

At Wonolo, our demand side is our customers. A typical customer is a logistics company with a warehouse needing Wonoloers (workers) to work on their production line.

The primary components of our Demand-side CAC are marketing and sales.

For illustrative purposes, let’s say the marketing component is $1,000 and the sales component is $4,000, making a total Demand-side CAC of $5,000. (Remember that these are averages and can vary widely.)

Jobs

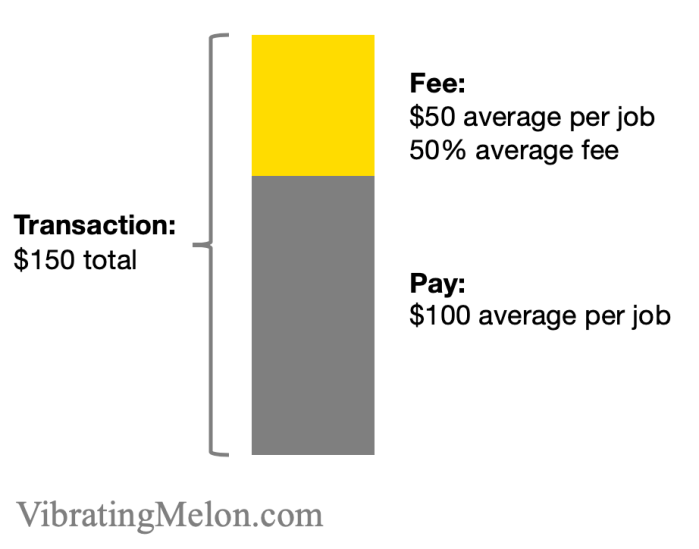

Our unit of interaction in our marketplace is the job. e.g. an 8 hour shift in a warehouse.

Length of shift and the hourly pay rate vary but, on average, let’s say a shift pays $100 and the average fee to our customer is 50%.

So, for each job, we charge the customer $150. We pass $100 straight on to the Wonoloer who did the job, leaving us with $50.*

Combining this with the CAC above, we can see that it will take the customer using Wonolo for 100 jobs to pay back our Demand-side CAC [$5,000 / $50]. This gives us some sense, but not a full picture, since it doesn’t include the time dimension or the Supply side.

*Staffing companies typically lead with their Gross Revenue, which includes the wages to be paid to the worker. I think this is a misleading “vanity metric” because the wages are simply passed through. At Wonolo, we lead with Net Revenue.

Demand-side Break-even Point

So, we know that it takes 100 jobs to recoup our Demand-side CAC. But, we don’t know how long that takes.

To calculate that, we have to know how frequently our customers use our service – frequency of interaction (also referred to as “frequency of transaction”).

Let’s say that, on average, our customers post 2 jobs (shifts) per day. We therefore now know that we recoup our Demand Side CAC after 50 days usage [100 / 2 = 50].

We also know that we hit our CAC-Doubling Point at twice this – 100 days.

Customer Lifetime & LTV

The next question we need to ask is whether we keep customers for at least 50 days. If we don’t, then we lose them before we pay back our Demand-side CAC, and our Unit Economics are negative.

Good news: we keep an average customer for 500 days. Easily long enough to recoup our Demand-side CAC.

We can also now calculate our Customer Lifetime Value (LTV). 2 shifts per day, at $50 per shift, for 500 days, is an average LTV of $50,000 [2 x $50 x 500].

Supply Side

So far, we haven’t considered the Supply side – in Wonolo’s case, our Wonoloers (workers).

In this approach, we’re going to model the Supply-side costs as Variable Costs incurred in delivering our service to our Demand side (customers).

How much Supply is needed?

The first question to answer is, how much Supply do we need to satisfy our Demand?

In Wonolo’s case – and since the “unit” we’re modeling is our Customer – the question is, how many Wonoloers do we need to do the work one Customer needs done?

The first answer might be to say we need one Wonoloer per shift. However, Wonoloers work multiple times for the same customer, so we don’t need nearly that many.

It turns out that, on average, a Wonoloer works for a given customer 10 times. So we only need 1 Wonoloer for every 10 jobs that our Customer needs done.

Supply-side CAC

Now we need to consider how much it costs us to acquire a Wonoloer.

There are two primary elements here: marketing cost (to get them to download the Wonolo app) and onboarding costs (to get them ready to work).

These costs add up to around $50 to find a Wonoloer and get them ready to do their first job. i.e. our Supply-side CAC is $50.

Impact of Supply-side CAC on Demand Side

Now we know how much Supply we need to satisfy a customer’s demand, and we know how much that Supply costs, we can put it all together.

For convenience, let’s look at a year.

Over the course of a year, a customer will use us for about 730 jobs on average [2 jobs per day for ~365 days].

So, on average, we’ll need 73 Wonoloers to meet that demand [730 / 10], and it’ll cost us $3,650 to acquire them [73 x $50].

Let’s look at how that impacts our overall unit economics calculations.

One approach is to look at the individual job level. It costs $3,650 to get the supply for our customer’s 730 jobs per year. So, per job, it costs us $5 to acquire the needed supply (Wonoloers) [$3,650 / 730 = $5].

Remember that we receive about $50 per job as our fee; so this means we’re spending 10% of that on Supply Acquisition.

So, rather than receiving the full $50 per job to pay back our Demand-side CAC, we’re netting $45 per job. This pushes back our Break-even Point by a corresponding amount. It takes us 111 days to hit breakeven on our $5,000 Demand-side CAC, once we’ve taken account of our Supply side costs [$5,000 / $45 = 111].

Given that we’re viewing the Supply side acquisition costs as variable costs, we can also say that our Contribution Margin of our staffing business is $45 per job and our Contribution Margin Ratio is 1.11 [$50 / ($50 – $5)].

Marketplace Dynamics

So, good news: it looks as if our business has positive unit economics! We break-even on a per customer basis after 111 days on average, even taking into account the cost of finding the needed Supply (Wonoloers).

However, because we’re looking only at one customer in isolation, this entirely misses the fact that Wonolo is a marketplace. These marketplace dynamics actually make the unit economics significantly better. This is one way in which marketplaces can be extremely powerful.

Remember we said that, on average, a Wonoloer works for a given Customer 10 times? That’s true but Wonoloers work at more than one Customer! It turns out that Wonoloers work on average for 10 different Customers during their lifetime on Wonolo.

Therefore, we share our Supply-side acquisition costs across multiple Customers.

This means we can divide the $5 per job that we spend by 10, meaning we only really spend 50 cents on average acquiring the needed Supply for one job [$5 / 10].

This means our Contribution Margin is actually $49.50 per job.

These marketplace dynamics exist in most marketplaces – arguably, that’s the point of the marketplace. Uber drivers don’t just drive one person, eBay sellers don’t just sell to one buyer, Airbnb hosts don’t just have one guest. The ability to “sell” the same Supply to multiple Demand is what makes a marketplace powerful.

Ignored Components

As I said at the outset, I’ve ignored some components of Wonolo’s unit economics that would be included in any full accounting. These would include items such as:

customer account management,

customer and Wonoloer support, and

payment network and banking fees to collect payments from customers and pay Wonoloers.

Negative Unit Economics and The Big Gamble

Everything I’ve described above discusses Unit Economics in a sober and rational way; which is often not the way Silicon Valley works.

There are several high-profile cases where companies have continued to grow aggressively despite clearly having negative unit economics. The poster-child arguably being Uber. At the time of writing (July 2020), despite its huge scale (meaning you’d expect its contribution margins would start to cover its fixed costs), Uber has never made a profit. Will it ever? We’ll see.

To continue to grow despite having negative unit economics, businesses have to continue to raise bigger and bigger gobs of money. Remember: negative unit economics means the more money you spend, the more money you lose. Uber raised a total of $24.5B, including over $9B in their Series G alone.

Investors in Uber are continuing to make a big gamble that there will only be one or two winners, and the winners will be those that capture as much of the market as possible, even if it is done at a massive loss. The thesis is that, once they’ve “won”, they’ll be able to keep out competition and control pricing to the extent that they can become profitable in the long-term.*

Investors are also gambling that Uber will be able to continue to raise money to cover the growing losses. Fortunately for them, their market timing was good and they were able to continue to raise bigger and bigger rounds at higher and higher valuations before IPO. If they were trying to raise that Series G today, it would likely be a very different story.

*This thesis is itself based on a perhaps flawed understanding of the strength of Uber’s network effects, but that’s a topic for another day…

Unit economics are critical to successful business growth. Without positive unit economics, spending more money means you simply lose more money.

However, when it comes to two-sided marketplaces, It’s Complicated™. I’ve seen experienced analysts admit defeat when trying to get to grips with our unit economics at Wonolo.

Here I aim to walk you through the topic step-by-step, in two parts. No prior knowledge is assumed.

Part 1: Unit Economics Basics

I want to provide a gentle learning curve. Before we talk about two-sided marketplaces in Part 2, let’s first quickly cover some basics. If (like me) you don’t have a formal background in finance, you may struggle with some of the terms used.

Disclaimer: because I’m assuming no prior knowledge, some complexities are overlooked for simplicity.

Ok, we’re talking about “unit economics”; so, what’s a unit?

For me, the confusion starts right here. As the name implies, a “unit” might originally have referred to a widget made in a factory. For example, if we run a factory that makes paperclips, unit economics relates to understanding the economics of paperclip production and sales, down to the level of an individual paperclip.

However, in the context of startups, we typically have one product and we’re selling access to that product. The “unit” we’re interested in modeling is the act of selling access to a user or customer.

Therefore, a “unit” is typically equivalent to a customer or user. As we run through these basics, you can think of our “unit” as a customer.

Variable vs Fixed Costs

The first core concept to understand is the distinction between “Variable” and “Fixed” costs.

Simply put:

“Fixed Costs” remain the same, however much you sell.

“Variable Costs” vary depending on how much you sell. If you sell nothing, Variable Costs are zero.

When looking at Unit Economics, we’ll mostly be interested in Variable Costs.

Introducing our Lemonade Stand

I’m going to use a Lemonade Stand as an analogy. It’s a simple but sometimes flawed analogy. (If nothing else, it presents an opportunity for some heart-warming pictures.)

For our lemonade stand:

“Fixed Costs” would be the costs of renting and operating our lemonade stand, and the pay for the person running the stand. They stay the same whether you sell 100 cups of lemonade or 0 cups. (Ok, I wouldn’t normally pay my kids to run a lemonade stand but this is just an analogy.)

“Variable Costs” would be the costs of the lemons, sugar, and water to make the lemonade. They vary with how much lemonade you sell.

Customer Acquisition Cost (“CAC”)

The first of many TLAs (Three Letter Acronyms) is “CAC” or Customer Acquisition Cost. This is what it costs you to acquire one customer.

The most obvious and common costs included in CAC are marketing costs.

There are various accounting practices and standards that determine what else is or isn’t included in CAC. For example, in some cases, CAC may include all or some part of the compensation paid to people directly involved in selling to customers.

[Don’t confuse CAC (Customer Acquisition Cost) with COGS (Cost of Goods Sold) – they are related and may essentially be the same in a simple software business but CAC is the important consideration in our unit economics analysis.]

Our Lemonade Stand

Let’s say we print fliers to advertise our lemonade stand.

These cost $1 each to print and each one brings 10 customers to our stand.

Our Customer Acquisition Cost (CAC) is $0.10 [$1 / 10].

LTV

Our next TLA is “LTV” or Life-Time Value. This refers to how much money you’ll make from each customer, on average, during their entire time being your customer.

LTV is often difficult for startups – especially in the early stages – because you don’t have enough data. For example, perhaps customers will stay on average 2 years or 10 years but, if the startup is only 18 months old, you don’t know yet.

However, as the company ages, you’ll start to see the average customer life-time level off (or “asymptote”) to a certain value.

A complication here is that LTV can either be discussed as “Gross LTV” which is simply the money you get paid by the customer, or “Net LTV” where the variable costs have been subtracted.

Net LTV will typically be much lower than Gross LTV. If you want to look good, use Gross LTV. If you want to really understand your Unit Economics, use Net LTV.

Our Lemonade Stand

We’re going to charge 25 cents for a cup of lemonade. Our stand is only open for 1 month during the summer (and only this year).

On average, each customer buys 4 cups of lemonade. Therefore our customer LTV is $1 [4 x $0.25].

LTV:CAC Ratio

By dividing the average Lifetime Value (LTV) of a customer by the average cost to acquire a customer (CAC), we get the LTV:CAC ratio.

This is a simple measure of the efficiency of our business model – it measures how much more money you get back from each customer versus the cost to get the customer.

Our Lemonade Stand

So, our LTV is $1.00, and our CAC is $0.10, so our LTV:CAC ratio is 10:1. Pretty good.

MRR

Our third TLA is “MRR” or Monthly Recurring Revenue. This is the average amount of money you get each month, from each customer.

MRR is very commonly used for SaaS companies since they tend to have fixed and predictable income from each customer, based on monthly billing of a fixed amount. e.g. $9.99/month, paid every month until you cancel the service.

As we’ll see later, marketplaces can have very different dynamics and MRR can be a much less useful measure. I’m including it here because it is very commonly used in the context of unit economics and provides a simple way to explain some of the following concepts.

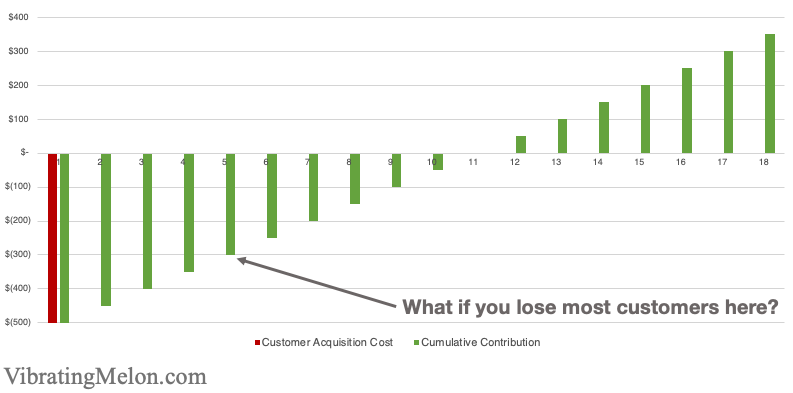

Break-even Point

As discussed above, the LTV:CAC ratio provides a simple way to understand the efficiency of a business model by comparing the money you make from each customer against how much money it costs to get them.

However, LTV:CAC ignores the time dimension: in many cases, you bear your CAC upfront but you only receive payment from the customer over time.

The Break-even Point refers to how long it takes a customer to “pay back” what it cost you to acquire them (the CAC).

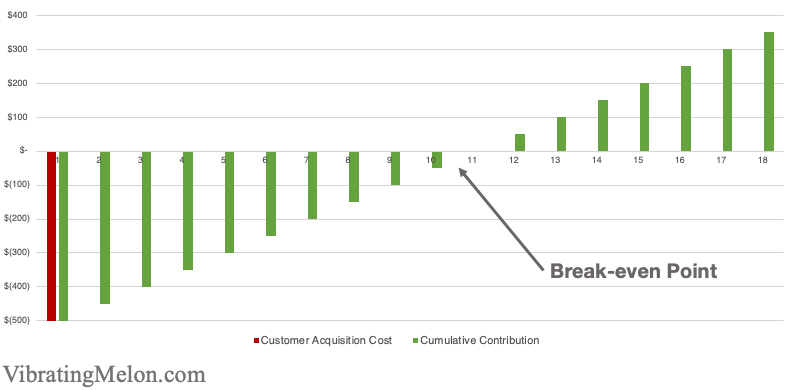

This chart shows a simple example of a company with a $500 upfront CAC and a fixed $50/month MRR. (i.e. a customer costs you $500 to acquire and pays you $50 per month for your services.)

As you can see, it takes 10 months to break-even in this simple case [$500 / $50].

Break-even Point is important because it determines how fast you can grow your business. While you’re waiting for a customer to “pay back” their CAC, you can’t use that same money to do anything else, like acquire more customers. (In finance terms, it impacts your “working capital”.)

So, the shorter your Break-even, the better.

CAC-doubling Time

Once you break-even on a customer, you’ve got your money back, and you can rinse-and-repeat. However, while you’re waiting to get your money back, your speed of growth is limited – you can’t grow any faster without more working capital.

One way to get more working capital is to raise more money from investors. With this money, you can spend it on acquiring more customers while you’re still waiting for your earlier customers to pay back their CAC.

The downside of this from a founder’s point of view is that you have to sell part of your company to raise more money, of course. The downside from an investor’s perspective is that they will have to keep putting more money in to increase the rate that you grow.

Therefore, it’s good to understand the CAC-doubling Point. This is the point in time where you’ve not only recouped the original CAC, but also earned enough to acquire another customer – i.e. 2x the CAC. Once you’ve got 2x your CAC back, you can continue to accelerate your growth without having to raise any more money from investors.

Simply put: your CAC-doubling point tells you how quickly one customer pays you enough to acquire another customer.

Churn

One of the biggest limitations on customer life-time value (LTV) is typically churn – i.e. losing customers.

To understand the impact of churn on your Unit Economics, you need to understand how frequently you lose customers (churn rate) and how much money they’ve spent with you on average before you lose them.

If they churn before paying back what it cost to acquire them (CAC), then you’re going to lose money – your unit economics are negative and the more you spend to acquire customers, the more money you lose.

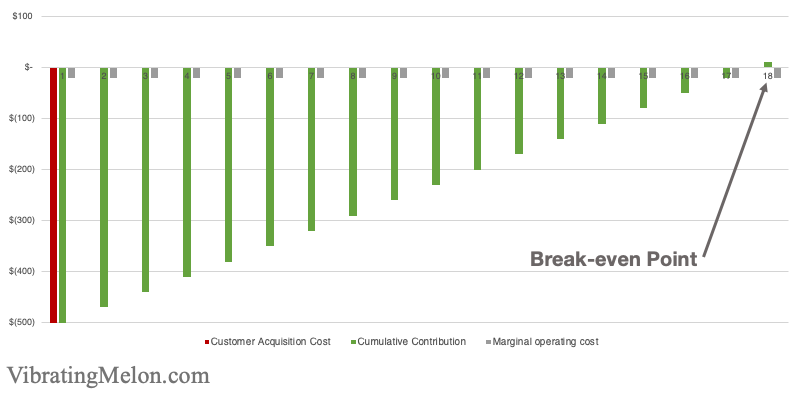

Marginal Operating Costs

Often there are ongoing costs associated with servicing a customer after you’ve paid your CAC to acquire them. Typical examples would be support and service/maintenance costs. Such costs are referred to as “Marginal Operating Costs”.

This is an area where finance conventions can differ but it’s easiest to think of Marginal Operating Costs as Variable Costs that occur over time.

From the perspective of Unit Economics, it’s important to understand the impact of Marginal Operating Costs on your Break-even Point.

The below chart shows the same $500 upfront CAC and $50 MRR but, this time, we’re adding a $20 marginal operating cost each month.

As you can see this pushes back the Break-even Point from 10 months to about 17 months. [$500 / ($50 – $20)]

Contribution Margin

Our final basic Unit Economics term is “Contribution Margin”. This refers to how much of the company’s fixed costs are covered by the revenue from customers, once the variable costs have been taken out.

Personally, I find the term confusing in the context of startups.

“Contribution Margin” is the contribution (hence the name) of a single product towards the company’s overall margin, whereas terms like “Gross Margin” refer to the company as a whole. i.e. if you sell only one product (like most startups), contribution margin and gross margin are essentially equivalent.

Contribution Margin is most often discussed as a ratio – “Contribution Margin Ratio”. It is simply the revenue divided by the revenue minus variable costs. Again, if you have one product only, “Contribution Margin Ratio” is equivalent to the % margin for the business as a whole.

Going Beyond Unit Economics

The ultimate objective is that, over time, your Contribution Margin (or margins, if you have more than one product) will be enough to cover all of your Fixed Costs.

At this point, you can think of your business as “profitable” as a whole, in colloquial terms – enough money is coming in to cover all of your costs (variable and fixed). In accounting terms, we’d also need to consider any costs related to taxes, interest on loans, etc before we can call it truly “profitable”.

Scooter unit economics: a Cautionary Tale

Now let’s take a look at a cautionary example in recent history.

In 2018, rental scooters suddenly appeared on our streets. Bird, for example, raised a $100M Series B and a $300M Series C – both in 2018.

So, scooter rental must be a great business, with great unit economics, right?

Let’s look at the unit economics of scooters:

Acquiring customers was not hard – people were literally tripping over them on the sidewalk (and complaining about it). So, for the purposes of this analysis, let’s say rider CAC was essentially $0.

It cost about $500 to buy one of those first-generation scooters.

Each scooter made about $500 per month in revenue.

The Marginal Operating Costs – charging, relocating scooters, etc – were about $200 per month.

So a Contribution of Margin of about $300 per month, per scooter. You can pay back that $500 purchase cost in less than 2 months. Pretty good business?

You may remember what happened: people didn’t treat the scooters kindly. The average scooter lasted about 28 days, so it wasn’t possible to recover the $500 upfront purchase cost before the scooter was destroyed, and the unit economics didn’t work.

The other thing that happened was injuries and subsequent lawsuits. A big proportion of scooter injuries were nasty head injuries, meaning big payouts for the scooter companies.

The huge amount of investment the scooter companies garnered was enough to maintain these losses for a while but ultimately a few things happened:

Scooter companies tried to source more resilient scooters, with higher longevity to get to breakeven on each scooter (compare how solid current [2020] scooters are with the first-generation 2017 Bird scooter).

Uber/Lyft acquired scooter companies – although the unit economics of scooters were poor, they provided a great way for ride sharing companies to acquire riders, and more cheaply. By becoming scooter chargers, it also allowed Uber and Lyft to offer additional income generation for their drivers.

Some scooter companies pivoted to electric bikes – much lower injury rate, much higher longevity, and much better unit economics.

The lesson of this story is that initial, quick takes on businesses can be misleading – you need to truly understand the unit economics.